The 2026/27 tax year begins on 6 April 2026.

Key take aways

- Taxes are increasing, but allowances aren’t. Accounts like your Octopus Money Direct Pension and Stocks & Shares ISA can protect and help grow your wealth.

- Investing your ISA allowance sooner rather than later has delivered higher returns, historically.

- Investing typically outperforms returns on cash, protecting the value of your money and growing it faster than inflation.

April 6: the birds are singing, the leaves are unfurling, and a fresh tax year has bloomed. We’ll leave the poetry there and focus on the finances, for everyone’s sake.

The start of a new tax year really can be exciting. Fresh allowances, taxes, and laws and the chance to plan accordingly.

Whether you made the most of last year’s allowances or not, you get a fresh start today. Below, we’ll explain your investment allowances for this year, tax updates, and the benefits of investing early.

Your allowances

ISAs

In total, you can save a maximum of £20,000 across all your ISAs in the 2026/27 tax year. Money you take out of an ISA, including any interest or returns you make, is tax free.

Whilst planning for your ISA allowance for this year, it’s also worth thinking ahead to next year too. From April 2027, if you’re under 65, you can still invest a total of £20,000 into your ISAs, but a maximum of £12,000 of your allowance can go into a Cash ISA.

Stocks & Shares ISAs are going to become even more important if you want to use your full allowance. Our 2025 Autumn Budget summary explains more.

Pensions

Your pension allowance is unchanged for the 2026/27 tax year. You can normally save up to 100% of your income or £60,000 (whichever is lower) across all your pensions.

Pensions are tax-efficient because you can use them to reduce your taxable income or get tax relief on contributions.

Changes to pensions are coming, but, for the 2026/27 tax year, there’s nothing new. As above, read our 2025 Autumn Budget article for more detail.

Remember, you can’t normally access your pension before the minimum pension age (currently 55, increasing to age 57 from 2028). You can only take your money from our pension as a single lump sum, with 25% of it tax-free. To take your pension using drawdown or another way, you’ll need to transfer it to another provider at retirement.

The early bird’s advantage

Investing at the start of each tax year, generally, gives you the best returns over the long-term. Trying to invest at the ‘best’ times or leaving it until the last minute can cost you.

Between 2015 and 2025, investing £10,000 into your ISA at the start of each tax year (rather than the end) would make you £21,200 richer today.

| Strategy | Total paid in over 10 years | Final ISA value, April 2025* |

| Early bird (invested 6 April) | £100,000 | £208,300 |

| Last minute (invested 5 April) | £100,000 | £187,100 |

*Estimates based on MSCI World net total return in GBP, April 2015– April 2025.

Figures include reinvested dividends.

This is down to three fundamentals

- A year’s head start: You get 364 more days’ growth compared to investing at year-end. As those returns compound over years, you enjoy a virtuous cycle of growth.

- Dividend returns: Investing your allowance early means you won’t miss any dividend payments.

- Good years add up: Stock markets have ended higher than they started in 6 of the last 10 UK tax years. If you wait, you could miss out on returns throughout those healthy years.

Nobody knows what the markets will do in the future, but history shows us that it’s been wise to invest early.

Remember, the value of investments can go up and down, so you may get back less money than you put in. Tax depends on your individual circumstances and the regulations may change in the future.

Tax changes in the 2026/27 tax year

UK tax revenues are the highest they’ve been since the early 1980s (roughly 39% of GDP). Income tax rates haven’t been raised, but other taxes have increased. As ever, tax rules may change and depend on your individual circumstances. You can find out more about the important allowances and tax rates for investors here.

- Personal allowances for income tax remain frozen until 2031. In Scotland, income tax bands have been tweaked slightly.

- Dividend tax has risen by 2% points (now 10.75% at basic rate, 35.75% at higher and additional rates).

- Your Personal Savings Allowance has stayed the same. Money you earn in an ISA doesn’t count towards your allowance and remains tax free.

Frozen allowances lead to what’s known as fiscal drag. This happens when rising wages or other income pushes you into a higher tax bracket, leaving you with less “real” spending power even though your salary went up.

Tax-efficient investing is only becoming more attractive.

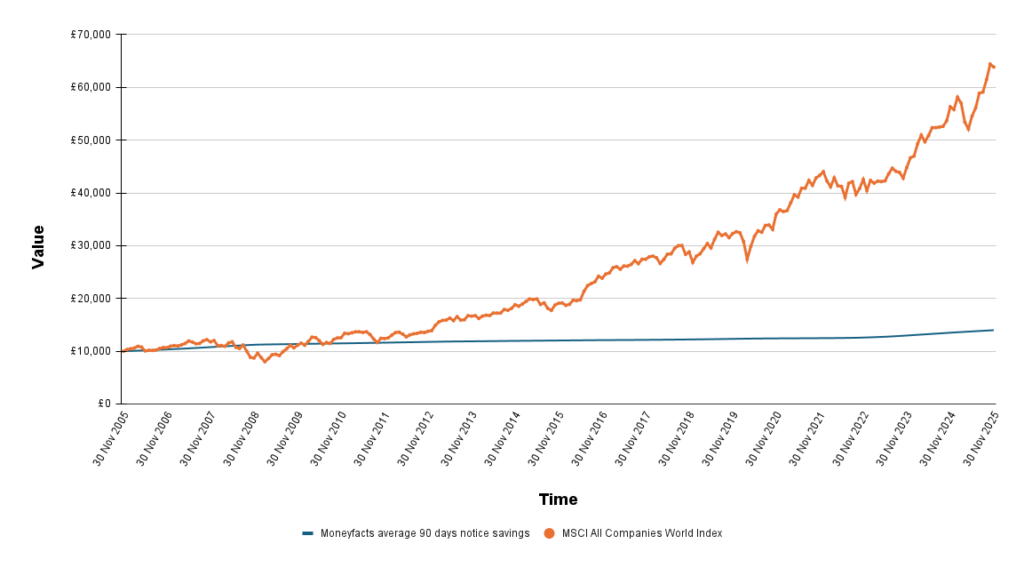

Balancing cash savings and Investing

Cash is good for short-term goals, where you need risk free savings with easy access. For long-term goals, cash savings may not keep up with inflation.

Historically, stock markets have generally grown more than cash savings over the long term. While markets have ups and downs, time in the market matters.

£10,000 invested vs. saved (2005 – 2025)

Source: Lipper, using Moneyfacts and MSCI. Remember past performance is not a reliable guide to future performance.

See our cash savings vs. investing guide to dig deeper into both options.Invest with confidence

This new tax year is another opportunity for you to get your money working hard. Leave it to grow and it can pay you back in the future.

Sign in to Online Service to make a one-off payment with your debit card or create/edit a regular payment.

If you need some expert help

With Octopus Money Direct you make your own investing and pension decisions. If you need help, Octopus Money (our parent company) offers expert financial planning and advice services. Additional charges may apply.

More resources and further reading

Manage your ISA – for more information about topping up and managing your Stocks & Shares ISA.

Managing your pension – straightforward explanations about key pension facts and rules.

Regular investing – Our guide that explains the superpower for growing your wealth.

Financial planning – Expert, personalised financial planning and advice from Octopus Money.

Register for Online Service – Start here if you haven’t set up access to Online Service yet.